Benefitting from a virtually unlimited influx of capital, sovereign wealth funds have quietly been ramping up their investments in startups worldwide.

A Powerful Force

Sovereign wealth funds, SWFs for short, are government-owned investment funds generally set up using a country’s natural resource wealth, fiscal surplus, proceeds of privatizations, or foreign currency reserves. The stated goal of these SWFs can be multiple but generally fall within three broad categories, clearly laid out by Orinola Gbadebo Smith:

- Stabilization priority: To insulate a given economy from internal and/or external shocks (investing in a variety of future-looking sectors such as AI, and renewables)

- A capital maximization priority: To transmute a given country’s natural resource wealth into longer-duration financial instruments for future generations (Norway investing its oil wealth in capital markets)

- Strategic development priority: To propagate development priorities such as job creation, infrastructure development, or economic diversification away from a single commodity (Gulf countries diversifying their income streams away from oil)

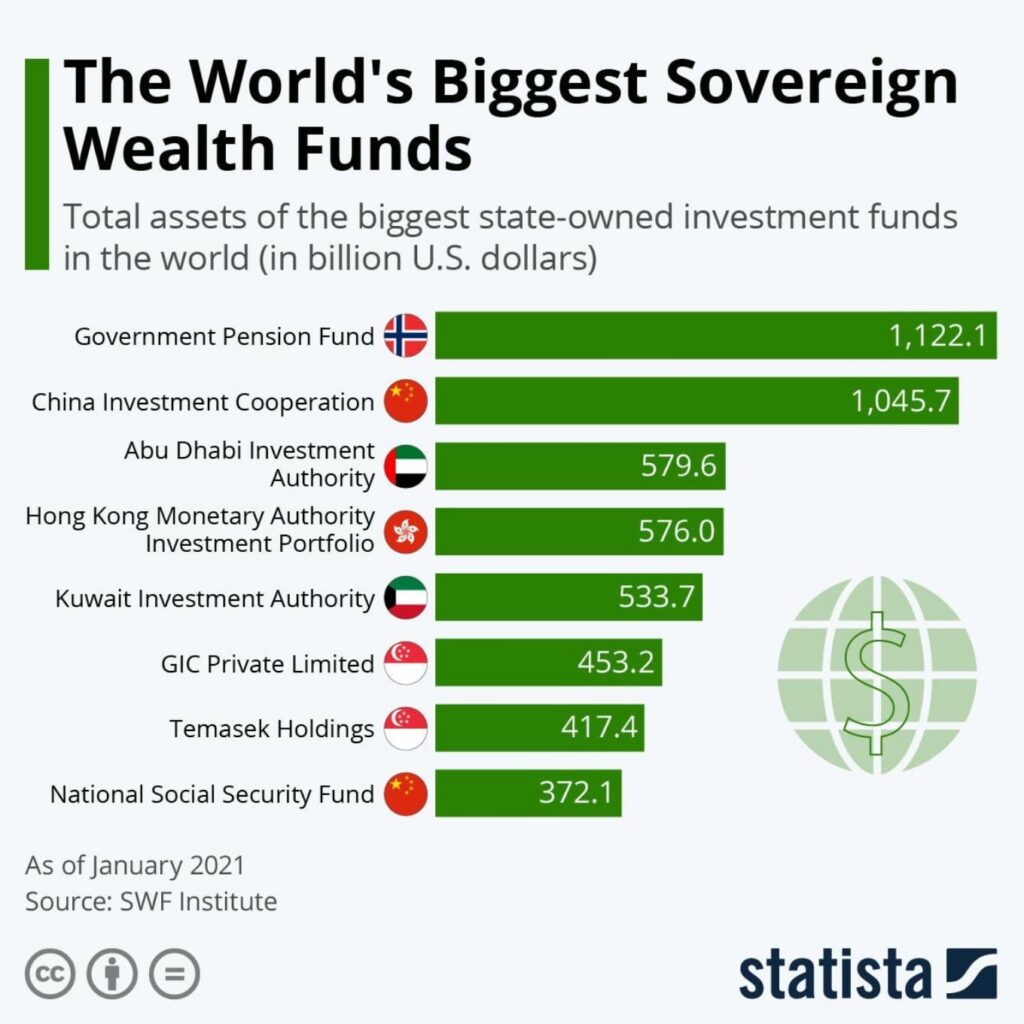

The SWF sector is highly concentrated, with 20 SWFs controlling 90% of the field’s assets under management (AUM). The masses of money handled by these SWFs are colossal, often counted in the hundreds of billions, even trillions in the case of the largest of them all, the Norwegian Government Pension Fund. They operate in somewhat of a grey, murky area, halfway between a potentially market-altering financial force and a half-veiled geopolitical tool.

“And there will be plenty of capital to go around — the report predicts that by 2030, sovereign wealth funds will manage a total of $17.7 trillion globally, up from $10.5 trillion in 2021.” – Source

SWFs enjoy a unique positioning within capital markets. They are mostly independent of the government that funds them (similar to a central bank), a provision established by the so-called Santiago Principles. Their only shareholder being the government, SWFs can allow themselves to pursue extremely long-term investment cycles, resulting in many adopting “contrarian” investment positions. For example, SWFs poured massive amounts of capital to save fledgling banks in 2008, a bet which turned into gold when the economy picked up.

SWFs invest in a variety of asset classes, including private and public equities, real estate, hedge funds, government bonds, corporate debt, etc. Their asset allocation largely depends on that particular SWFʼs goals. Funds with higher payout rates, such as pension funds, will tend to be more conservative in their investment style, while funds with a stated diversification goal, such as oil-money-powered ones, will tend to take more risks.

Talking about risks, more and more SWFs have been dipping their toes (and now their entire feet) into the world of venture capital, either by becoming LPs in funds or by directly investing in startups themselves. This trend has been growing over the past couple of years, but doesnʼt make much noise, given the traditional secrecy of these funds. The rate at which their appetite for startups is growing deserves a closer look though. Indeed, in 2021 BCG repored that state-owned investors invested $14.9 billion into more than 250 startup deals—more than double the number of deals in 2020.

Startups Galore

When looking at the numbers, the arrival of SWFs into the venture capital world is akin to a bull entering a china shop. Take GIC, Singaporeʼs sovereign wealth fund, for example. In 2017, GIC invested around $500M in European startups. Just 4 years later, that number had grown tenfold, reaching $5.5B in 2021. In 2022, an extensive report published by Global SWF, an intelligence firm focused on SWFs, even named venture capital as ʻasset class of the yearʼ. So why is it that traditionally long-term thinking, precautious and measured mega-investors have speed-run the venture capital world?

The reason is the same reason I started this newsletter in the first place. Namely the almost unfathomable surge of startup activity worldwide and with it, the decoupling of financial returns from geography. 2021 was a potent exemplification of this trend, with virtually every region in the world raising record levels of VC funding. For SWFs, many of them located in emerging markets such as Asia and MENA, it is unsurprising that the startup boom in their regions and worldwide caught their eyes.

SWFs are expressing more and more interest in startup investing for two main reasons. The first is that the number of startups and the subsequent number of exits is increasing, especially in emerging markets. Take India, for example, where SWFs have participated in the country’s roaring IPO market by becoming so-called ʻanchor investorsʼ, investing large sums just before startupsʼ IPO. The second reason is that companie are staying private longer, elongating the timeframe in which SWFs can invest, especially in large, late-stage rounds.

“In July, food delivery company Zomato went public with $600M gained from 186 anchor investors, including ADIA, CPP, GIC, and OMERS. Temasek had invested in its Series J in 2020 – and likely achieved a big return on exit. Also in July, e-commerce platform Flipkart raised US$ 3.6 billion with a new funding round that included ADQ, CPP, GIC, Khazanah, and QIA, consolidating its position as India’s largest unicorn. Other Indian unicorns chased by SOIs (State-Owned Investor) included Byjuʼs, Ola, Delhivery, PolicyBazaar, and Sharechat.” – Global SWF

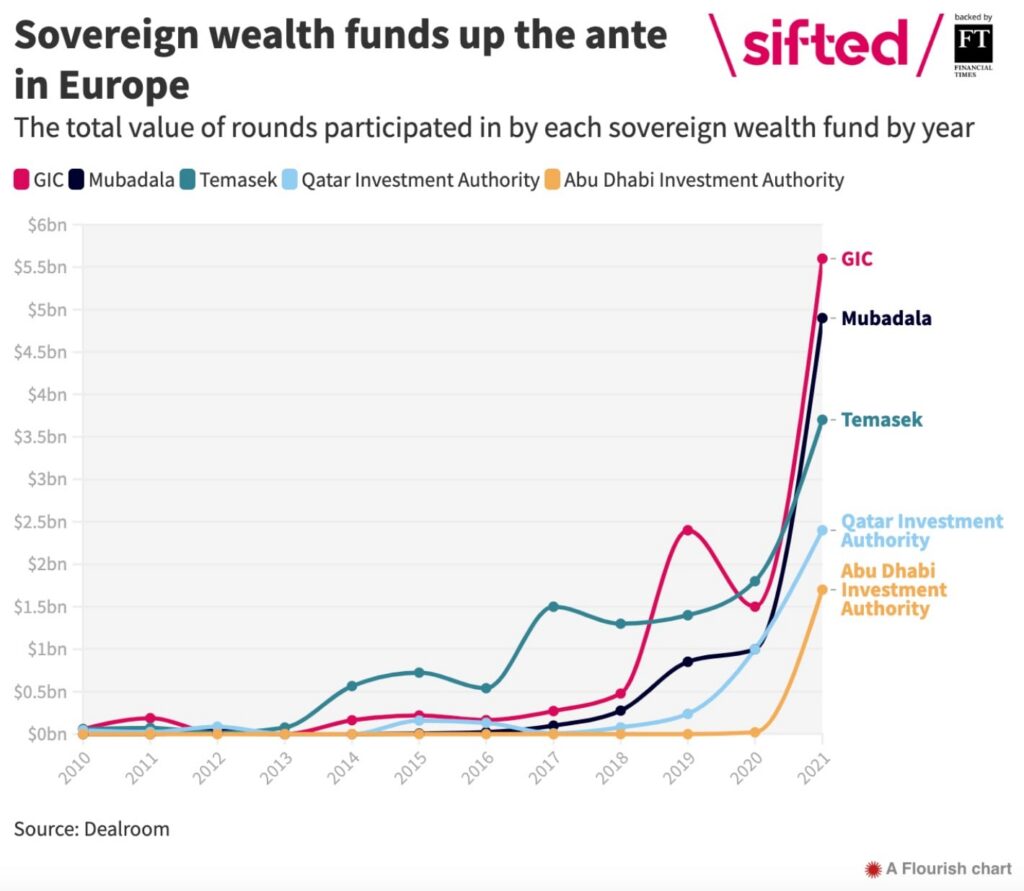

The thunderous entrance of sovereign wealth funds into the VC world SWFs involvement in Europe, a fast-growing startup region, is a testament to what could happen to other embryonic startup ecosystems such as Africa (image source)

Singapore: The SWF OG

When it comes to investments in startups, Singaporeʼs two main SWFs, GIC and Temasek, take the crown, followed by the UAEʼs Mubadala. Since 2018, returns from Singaporeʼs SWFs have even become the biggest contributor to the country’s budget. How is a small country of 5.5 million people, with virtually no natural resources, playing such a prominent role in funding the current global startup revolution?

Let’s start with GIC. Established in 1981, GIC is Singaporeʼs official SWF, tasked with investing the country’s foreign reserves in markets abroad to make it grow. In 1986, the company established its San Francisco offices to gain a foothold in the American VC market. Since its founding, GIC has invested around $254B in venture capital, investing directly into VCs, startups, or alongside renowned names such as Sequoia or Andreessen Horowitz. Some rockstars in GICʼs portfolio include but are not limited to DoorDash, Affirm, Nubank, and Klarna, as well as a slew of Chinese heavy-weights such as Meituan and Alibaba. Recently, GIC led cryptoʼs Chainalysis Series F investment.

Temasek was established in 1974 with a slightly different mandate. The goal of Temasekʼs creation was to create a standalone investment company, with the government of Singapore as the sole shareholder, to manage and grow the assets held by the Singaporean government at the time.

Contrary to GIC, the goal wasn’t to explicitly grow foreign reserves by investing abroad but rather to transfer the management of Singaporeʼs assets to professionals while letting government officials focus on public policy. Inheriting from a $354 million war chest in 1974, Temasek now manages a globally distributed and diversified $284 billion portfolio, generating an average 14% total shareholder returns.

When it comes to SWF VC investing, Temasek ruthlessly dominates, disemboguing $5.1B into the asset class last year, followed by fellow Singaporean GIC at “only” $2.1B. The impact of Temasekʼs firepower on the Asian startup ecosystem is particularly interesting. The Singaporean behemoth was involved in virtually all Indonesian startup successes, from Gojek to Tokopedia, to Grab, etc. For a region where founders often struggled to raise venture capital, the arrival of deep-pocketed SWFs is a boon.

I personally predict a similar situation happening in MENA, where the Gulf statesʼ SWFs will, and already are, kickstarting the next generation of Arab unicorns after decades of venture capital scarcity.

SWFs – Some Key Characteristics

In this last paragraph, I want to explore a couple of SWFsʼ key characteristics in order to better comprehend the sector and how it might evolve over the next couple of years.

First, SWFs are taking a more and more proactive approach to venture capital, a harbinger of them playing a more potent role in the VC world. While previously satisfied with investing in VC funds as LPs, SWFs are now actively scouting startups themselves, investing earlier, and even creating their own standalone VCs, such as Taiwania Capital, bankrolled by Taiwanʼs SWF. A more vigorous venture capital industry will translate into more deals, but more importantly, better terms for founders. SWFs are also attractive to founders, given the doors their relationships can open.

Second, I wonder if we are going to start seeing an overlap between geopolitical tensions and the startup world. While startups have been affected by them on a macro-scale, the prominence of SWFs in startupsʼ cap tables will give founders one more variable to consider when raising funds. Indeed, while “independent” in their investment strategy, SWF will always inevitably be tied to a government and its subsequent foreign policy agenda. This factor adds extra complexity when raising from these investors, as founders who do so will inevitably be tied to a sovereign state whether they like it or not.

Thirdly, I think the case for SWFs in the startup world is particularly interesting in the context of a “financier of last resort”, which they were in the 2008 crisis. SWFsʼ long investment horizons enable them to be contrarian, investing where traditional investors are frisky. This strategy could have an outsized impact on emerging ecosystems such as Africa, where the nominal amount of VC capital raised is still embryonic despite media fanfare.

To give you an idea, the entire continent of Africa raised $5.2B in VC last year, while the country of France raised $11B. My point here is that much more capital has yet to be deployed in emerging markets, and SWFs could have a first-row seat by taking ambitious bets.

Finally, SWFs can provide an interesting alternative to founders. Indeed, most of those SWFs have been actors in almost all categories of the VC world, either being LPs in funds or creating one. This confers them with a unique global network to tap into. Furthermore, the seemingly endless war chest and long-term agenda they hold might enable founders requiring patient capital, such as deep-tech/hardware ones, to access a welcome alternative to VCs excited about the next 15-minute delivery startup.

Singaporeʼs dominance is quite remarkable. For the remainder, the entire country of Singapore is half the size of Bangkok. (image source: GlobalWF)

Conclusion

In my opinion, the quiet, discreet, but definitive entry of SWFs into VC is a testament to the incredible potential startups worldwide represent for investment professionals. The case of Asia and the growing maturity reached by pioneering ecosystems such as Indonesia are a blueprint for what the next decades hold for other ecosystems such as MENA and Africa. Used to investing at the very frontier, SWFs and their deep pockets will be key protagonists in financing the global startup revolution we are currently experiencing. Let’s see how traditional VCs react.