by Adrian Garcia-Aranyos

After being tapped to lead its Spain operations, Adrian Garcia-Aranyos became president of Endeavor in 2019 and has been running the organization ever since.

Endeavor is a leading global community of high-impact entrepreneurs. Cumulatively, Endeavor entrepreneurs have created more than 4M jobs, raised $60B in equity funding, and generated more than $50B in revenue.

Prior to that, Adrian held several executive roles at J.P. Morgan Chase & Co; The Economist Newspaper Group; and CM Capital Markets.

A Different Breed

Over the past two decades, Endeavor has supported founders from over 30+ countries. We have seen the rise and flourishing of new startup ecosystems around the globe. As I’ll explain later through our “Multiplier Effect” theory, an ecosystemʼs takeoff often starts with a couple of brave souls.

An ecosystemʼs first unicorn, such as Rappi in Colombia, or first major exit, such as Paystack in Nigeria, is often if not always the hardest. By definition, an ecosystem has a terribly hard time attracting local and international investors if it has no exit to show for. And, logically, a newborn ecosystem has no exits to show for.

This is akin to a cold start problem. One that requires truly exceptional entrepreneurs to resist the siren call of launching their company in a more developed ecosystem. I’ve found this type of founder, the ecosystemʼs first generation, to be truly inhabited by their companyʼs mission. When funding and support are absent, conviction and grit take their place. These founders arenʼt in it for the money: the odds of success are simply too low.

As new capital sources gain interest in startups (DFIs, private equity, governments), these founders master the cra of mixing funding sources from the get-go. Grants, angel investors, loans, public money, private money… In a nascent ecosystem, funding sources are so scarce that anything goes.

Kavak (Mexico), Careem (UAE), Insider (Turkey), Go1 (South Africa), Grab (Singapore), MercadoLibre (Argentina)… We’ve put together a global interactive map of all of those momentous companies.

The ones that have managed such a feat are rare. But their rarity exacerbates both how hard it is as well as the downstream impact they have had on their ecosystem.

Sources: The Big Deal, AVCA, Crunchbase, LAVCA, Tech in Asia

The Multiplier Effect

Endeavor defines the Multiplier Effect as follows: the compound, exponential impact a founder has on the entire entrepreneurial economy of a region when they mentor, invest in, and inspire the next generation of entrepreneurs.

Startup “ecosystems” are aptly named. Everything and everyone is, near or far, related to each other. When an ecosystem experiences a first startup success, a term we will refine below, a couple of crucial elements occur.

First, the employees of said company are now armed with an arsenal of operational, and in the case of an exit, financial resources. Bright employees from an ecosystemʼs first success go on to found their own startups. And often, they are joined and financed by their former colleagues. That forms a virtuous circle. It is what, rather barbarically, is referred to as “mafias”.

Second, in the case of an exit, the ecosystem gains instant credibility points with the investor community. Careemʼs $3B+ exit to Uber most definitely redefined the regionʼs startupsʼ attractiveness to foreign and local capital alike.

Third, and probably most important, a startup success reshapes the local mentality. In many young ecosystems, local talent has to be convinced that, yes, they can create great companies at home. A startupʼs success also helps to vindicate working or launching a startup as an acceptable societal choice. This remains a major barrier in ecosystems where entrepreneurship is sometimes viewed as the result of not finding a job.

The combination of these three elements is what Endeavor likes to call “The Multiplier Effect”. That’s why we’re focused on quality, not quantity, picking and supporting the minute number of companies that we believe can spark that Multiplier Effect.

A final point about what “success” means in this context. While the majority of companies contributing to the Multiplier Effect tend to have a happy financial ending, failed companies can also render a net positive. I am thinking of Airlift in Pakistan, for example.

While the company ultimately failed and closed down, the amount they raised, the talent they formed, and the youth they inspired have certainly left an enduring, positive mark on the Pakistani ecosystem. That’s priceless, no pun intended.

Our obsession with unicorns

We believe that unicorn status is an elegant yardstick, a way to easily identify companies that have scaled and hold incredible promise. The “unicorn” category is also useful for research purposes: we just released our “Unicorn Pathways” report, which seeks to dispel myths about unicorn foundersʼ backgrounds. Hint: they seldom are geniuses in dorm rooms.

The average founder had 10 years of work experience.

There are no shortcuts on the pathway to building a unicorn company. The unicorn founders included in this study gained a decade of experience following their undergraduate education, on average. Several existing studies have shown that the quintessential successful founder is not particularly young or a college dropout. Endeavour’s research builds on these findings, showcasing that successful founders usually gain entrepreneurial experience and build networks over time.

What is nefarious, however is the industry’s obsession with valuation as a definitive measure of success. As the current funding winter has demonstrated, valuations are the only metric that founders don’t control. Cases such as Klarna, or more tellingly, WeWork, demonstrate that valuations are nothing more than semi-educated guesses.

Fixating over the valuation KPI is thus a futile exercise for founders. The improvement of key business fundamentals should always be the plat du jour. The startup industry should avoid using valuation as the celebration of a founderʼs success. If anything, valuation is the most nebulous measurement one can find.

The diasporaʼs essential role

One of the study’s main takeaways is the global-minded nature of unicorn founders, especially in emerging markets. This, in turn, is conducive to a trend we are increasingly seeing in the sector: south-south startup acquisitions. Mexican unicorn Kavak buying a competitor in Oman comes to mind.

What this also implies is that in young ecosystems, the diaspora is an invaluable resource. Statistically, there’s a great chance that the founder that will kickstart the ecosystem is a returning diaspora. Engaging them is more of an art than a science.

While Endeavor does its best to lay the groundwork for such diaspora-driven initiatives through our Greek and Lebanese offices, for example, the buck ends with a few daring individuals willing to make the jump. You need to convince the visionaries.

That’s also why we use our Multiplier Effect as a selling point: by coming home, you arenʼt just starting a company but potentially kickstarting its entire ecosystem for years to come.

Conclusion

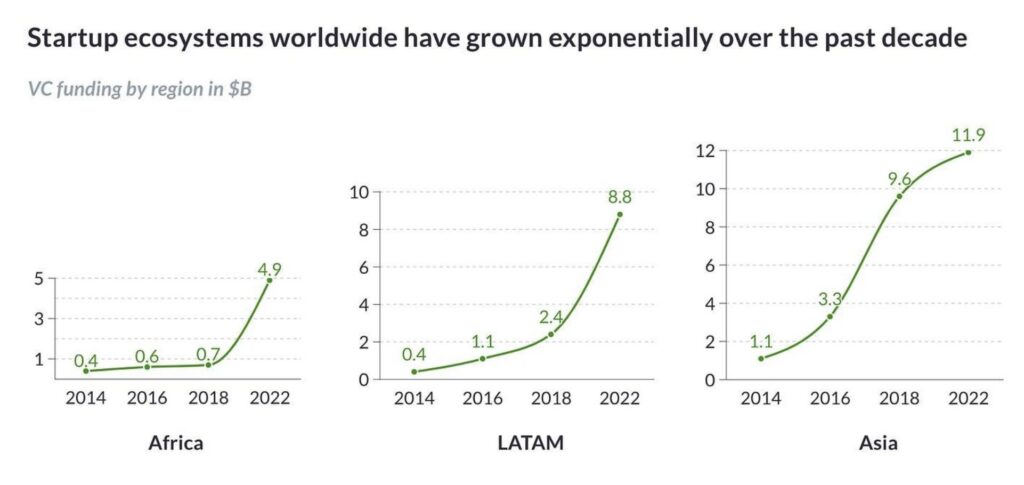

Carried by cheap money, 2021 saw a strong uptick in VCsʼ interest in startups outside of their home geographies. Pertinent theses surrounding the inevitable digitalization of emerging markets helped strengthen the investment case. We saw American VCs investing in Africa, Japanese VCs investing in LATAM, and Britsh VCs investing in Asia… The globalization of the startup world seemed complete.

2022ʼs lot of geopolitical surprises, combined with a jolly mix of inflation and high-interest rates, drastically tempered VCsʼ international proclivities. While some see the departure of so-called “tourist investors” from their home geographies as definite, I tend to believe rather the opposite: the genie is out of the bottle.

For starters, some American VCs, such as General Atlantic, have maintained their presence and activity in LATAM, despite the funding winter. We’re also starting to see emerging market-focused VCs close substantial fund sizes, such as Partechʼs recent $250M Africa fund. Similar announcements could relaunch broader VC interest in these markets, the sector’s herd mentality being an open secret.

The funding winter has contributed to correcting and cooling valuations that had indeed gotten out of hand. While I’m not affirming that 2021ʼs euphoria will reappear next year, the much-publicized “dry powder” VCs still hold will have to be deployed sooner or later.

The best way for emerging market founders to attract some of that booty is and will always be to show exit potential.